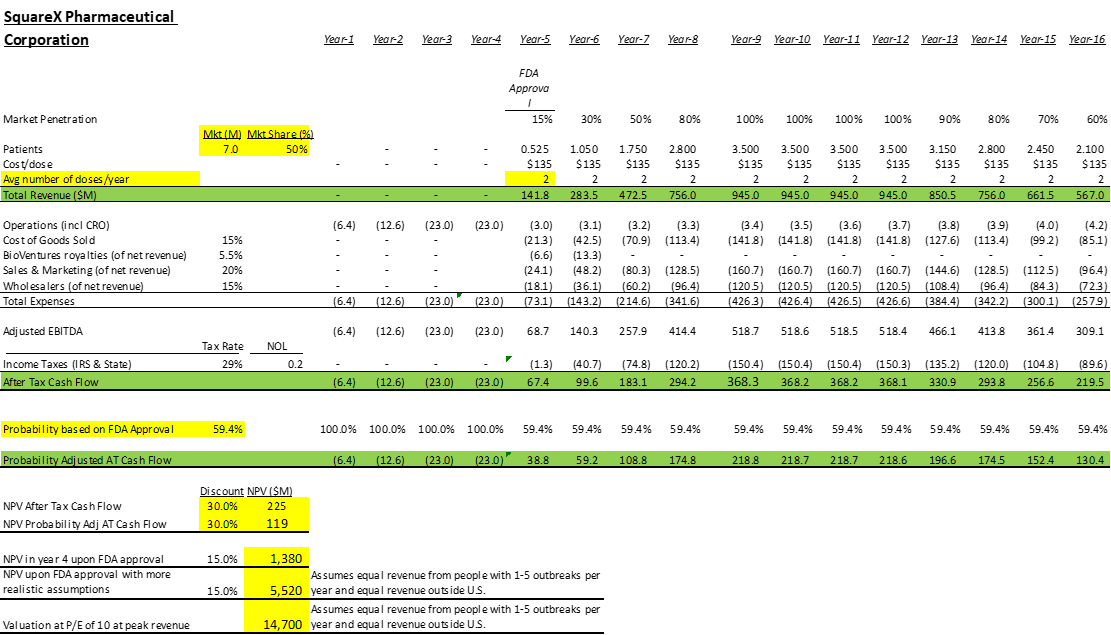

The valuation model following gives a Net Present Valuation of Squarex of $119 million using extremely conservative assumptions.

The key assumptions of the model are

- No sales outside U.S.

- No sales to persons with fewer than 6 cold sore episodes per year.

- Treating 50% of U.S. persons with 6 or more outbreaks.

- Sales of 2 doses per year on average to those persons instead of the recommended four doses.

- Four years to FDA approval. We think three years is feasible.

- 59.4% chance of FDA approval, which is the historical norm for drugs after Phase 2. In our case, the drug has been effective in 3 of 3 clinical trials with no serious adverse events, so we think the chance of FDA approval is actually higher than that.

- Discount rate of 30%. That is high. 25% would be more reasonable and would result in a higher valuation.

- $135 per dose. We conducted a survey of pharmacy benefit managers, and they all said they would approve reimbursing for this drug and the average reimbursement level was $135 per dose. We feel this is a conservative estimate, relatively low pricing for a prescription drug taken just four times per year.

Those assumptions are all conservative. In particular, it is reasonable to assume that sales to people with 1-5 outbreaks per year will be approximately the same as to persons with 6+ outbreaks and that foreign sales and profits will be about the same in total as U.S. sales. Those two changes would quadruple the valuation

The model also assumes no revenue from sales for other diseases, and we plan to seek FDA approval for other diseases.

Once we have FDA approval, nearly all the risk has been removed and the the sales from that point forward would be fairly certain. A fair valuation at that point, in three to four years, would be over $1 billion just based on U.S. sales to persons with 6+ outbreaks per year only.

Including revenue from persons with 1-5 outbreaks (assumed as equal to revenue from the fewer people with 6+ outbreaks per year) and including foreign revenue (assumed as equal to U.S. revenue) would quadruple that valuation to $5.5 billion (250 times the stock price of this offering).

At a P/E of 10, at projected peak revenue (including foreign revenue and revenue from people with 1-5 outbreaks per year) the market value would be $14.7 billion, 650 times the current valuation for this offering. And that still does not include revenue for any disease other than cold sores.

Thus, an increase of valuation from $22 million at the share price of this offering to about $5 billion after FDA approval in four years or less, and a 100-fold return for investors at $3.00 per share, seems quite possible.